About 25 years ago, I visited a forest in Belize where US and Canadian energy companies were paying a landowner not to harvest trees. The idea, which was borderline radical back then, was that carbon emissions from energy generation in North America would be “inhaled” as carbon dioxide (CO2) by trees in Belize, essentially offsetting the impact of the pollution.

Fast forward to today, where that same idea has taken root in West Virginia and across Appalachia, in a big way: nearly a million acres in West Virginia alone are now enrolled in forest carbon projects. New programs and types of forest carbon projects are opening up opportunities for more landowners, including those with very small holdings, to participate in forest carbon markets which diversify revenue potential.

The basics: trees are made of wood and wood is a form of stored carbon, like coal or gas. About half of wood’s dry mass is carbon, regardless of tree species. Through photosynthesis, trees take in carbon dioxide, retain the carbon, and release oxygen back into the atmosphere. Much of that ‘sequestered’ carbon is stored as wood, comprising the bole and branches of trees, the support system that enables trees to grow up and out to harvest even more sunlight. The average acre of mixed hardwood forest in West Virginia can sequester 3–5 tons of carbon (or, CO2 equivalent) per year. These tons then comprise carbon offsets — that are sold as carbon credits — which are used to mitigate the impacts of burning fossil fuels.

Currently, there are three main types of forest carbon projects in the US: Afforestation/Reforestation, Avoided Conversion, and Improved Forest Management. Afforestation/Reforestation projects rehabilitate degraded lands through tree planting and other silvicultural practices to restore forest cover. Avoided Conversion projects aim to keep standing forest carbon stocks intact, preventing the conversion of forests to other land uses. Improved Forest Management (IFM) projects are by far the most common project type in West Virginia. IFM projects recognize typical forest management practices in a region and then aim to “improve” upon them for achieving carbon objectives. The primary means of increasing carbon sequestration through IFM projects is by deferring timber harvests, thereby extending rotation lengths.

For the last decade, most forest carbon projects required a commitment of 40–100 years; to withdraw before then triggered significant financial penalties. Today, however, new forest carbon programs are emerging with much shorter time frames, some requiring enrollments as short as one year. With longer-term commitments, land can be bought and sold and the forest carbon project requirements stay with the property.

A common misconception about forest carbon projects is that they all prevent harvesting. Some do, such as Avoided Conversion projects. However, IFM projects, which are most relevant to West Virginia, allow landowners to choose one of four courses of action:

- Do not cut but sell the volume of annual forest growth as carbon offsets;

- Cut and sell the volume of annual forest growth as timber, into forest product markets;

- Some combination of 1 and 2, selling some timber and some carbon offsets; or

- None of the above, no obligation to cut trees or sell anything.

Note that the decisions center around a forest’s annual growth, which is already widely accepted as the basis for sustainable forest management of any kind. Forest carbon projects unlock markets that provide optionality for landowners to generate revenue from different sources, sometimes concurrently.

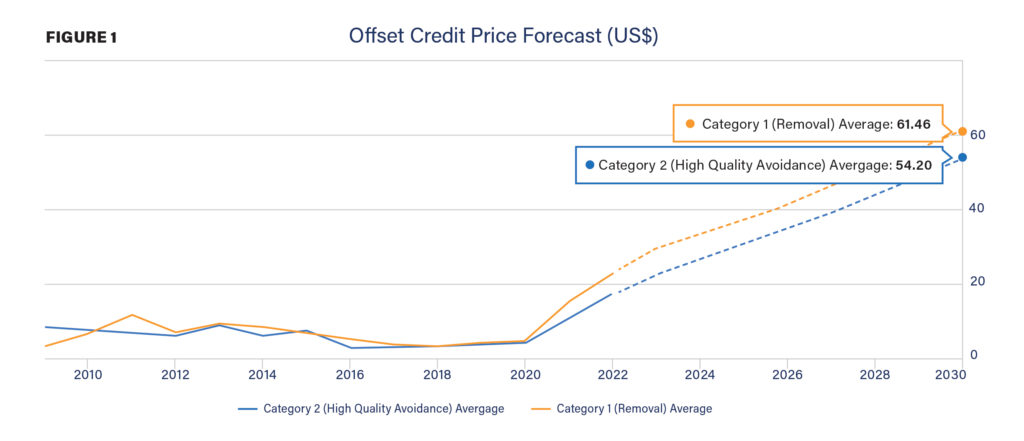

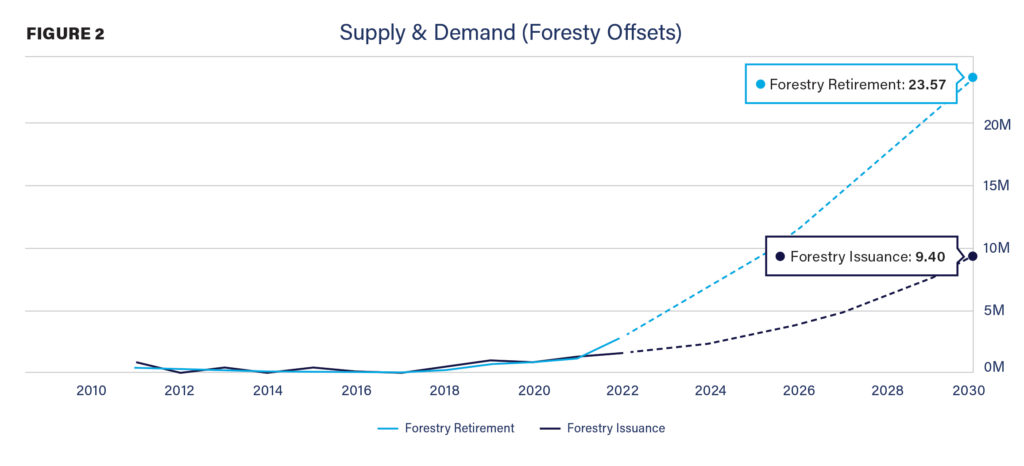

The markets for forest carbon credits, like many other facets of climate change mitigation technologies, are evolving rapidly. There are two broad categories of markets, based on the methodologies used in developing the project: compliance and voluntary. The US compliance or regulatory market is dominated by California’s program with the state’s Air Resources Board (ARB). Carbon-emitting companies located in California are compelled by state law to reduce their CO2 emissions or offset them with carbon credits. Then, there are more diverse voluntary markets, with varying sets of rules and requirements. Large corporations are one example of a buyer purchasing voluntary carbon credits to offset their carbon footprints to address stakeholder/shareholder interests. Until recently, credits within the ARB system commanded higher prices. Now, however, that is changing quickly as demand for forest carbon credits begins to exceed the available supply (Figure 1). While both ARB and voluntary credits may range between $8–$15 per ton today, prices are projected to rise to $50–$70 by 2030 (Figure 2).

Do carbon credits compete with timber? Sure, that’s the point after all, deferring harvests while storing carbon on the stump. Until recently, however, carbon prices generally were lower than any forest products prices on a per cord or per ton basis, minimizing financial incentives to avoid cutting timber. Now that is changing as carbon prices rise to levels that compete with the lower ends of conventional timber markets. For example, $8/ton for carbon credits is approximately equivalent to about $25/cord for pulpwood (min. 5” dbh). So, as carbon prices go above this level, a landowner may make the rational decision to harvest less pulpwood and instead sell carbon credits. At $50/ton, carbon begins to compete directly with hardwood sawtimber (min. 12” dbh).

These are exciting times for foresters and forest landowners, especially in West Virginia where growth rates in natural forests are robust and carbon sequestration is high. While the concepts of forest carbon as a management goal and a marketplace have been around for decades, it’s only in the last few years that they have begun to take off in the Appalachian region. No doubt there will be new and interesting changes as forest carbon projects and markets grow and evolve in West Virginia and beyond.

{kind=link}