INTRODUCTION

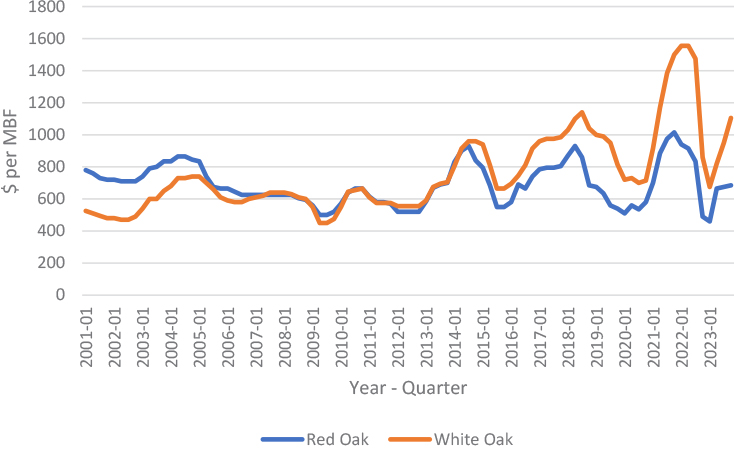

The grade lumber component of the hardwood sawmill industry is continually faced with cyclic fluctuations in lumber pricing. Predictability of grade lumber markets, with any level of confidence, is uncertain at best. Figure 1 illustrates the volatility in nominal pricing of 1 Common red oak and white oak lumber over a 22 year period (2001 through 2023), on a quarterly basis. The data points represent Hardwood Market Report1 pricing from the second week report for January, April, July, and October. For red oak and white oak, the period from 2004 through 2013 showed a downward trend in pricing, followed by significant peaks and valleys until 2021 and then a drastic increase in price followed by a deep drop and another spike in 2023.

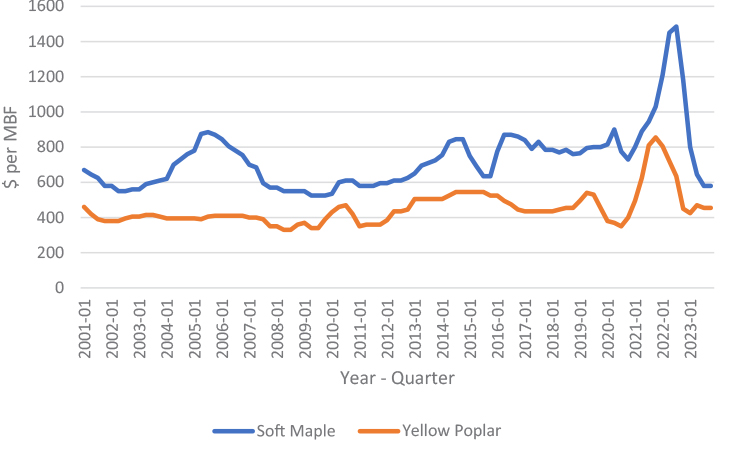

Figure 2 illustrates the volatility in nominal prices of 1 Common soft maple (unselected) and yellow-poplar lumber over the same time period. Yellow-poplar exhibited much more stable nominal pricing from 2001 through about 2021 and much more stable than soft maple, red oak, or white oak. Soft maple showed a bit more stability over the 2001 through 2021 period than red oak and white oak. Both yellow-poplar and soft maple experienced drastic swings in price starting in 2021, much like red oak and white oak.

Over the entire time series (first quarter 2021 to fourth quarter 2023) No. 1 common yellow-poplar had the least volatility with a nominal price range of $330–$855 per mbf or $525 per mbf. During the same period red oak experienced a nominal price range of $460–$1,015 or $555 per mbf, white oak ranged from $450–$1,555 per mbf or $1,105 per mbf and soft maple (unselected) ranged from $525–$1,485 per mbf or $960 per mbf.

Together Figures 1 and 2, create a picture of continual fluctuations in price with significant price swings from late 2020 through the end of 2023. Managing this volatility is a significant challenge for hardwood sawmills and represents an ongoing threat to their continued economic viability. This level of uncertainty places considerable pressure on stumpage pricing, where mills must try to predict lumber pricing up to two years in the future for stumpage purchases today. Rising lumber prices over time can mean relatively good returns on stumpage purchased today, but falling lumber prices can have devastating impacts on overpriced stumpage prices today.

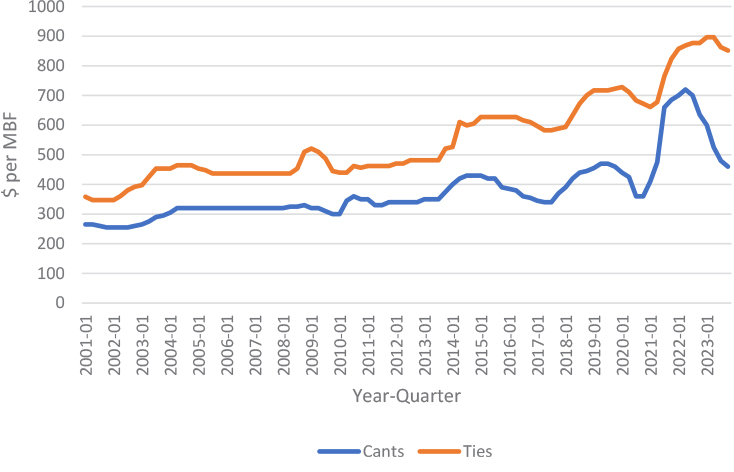

Alternatively, Figure 3 illustrates the trends in pricing for both pallet cants and railroad ties. The obvious difference is that pallet cant and tie prices, while showing some peaks and valleys, exhibit a general upward trend, with tie pricing always exceeding pallet cant pricing. The consistent upward trend was interrupted at the end of 2020 when all lumber related markets experienced wide swings in nominal pricing. One takeaway is that a degree of certainty in pallet cant and tie pricing, not seen in grade lumber, is evident. The question is how best to take advantage of this situation?

When the hardwood industry is mired in another down cycle for grade lumber, can hardwood sawmills offset some of the pain by producing railroad ties? The answer lies in better understanding how tie pricing can affect profitability for various combinations of log size (diameter) and clear faces.

The WVU Appalachian Hardwood Center (AHC) has, over the last decade plus, conducted over 60 sawmill studies throughout the Appalachian Region. These studies collected data on individual logs, where each log was measured and characterized according to a number of variables, including scaling diameter, length, scaling defects, as well as a number of other variables and then numbered on each end. The logs were then processed through the sawmill. Each board was graded and scaled, and the dimensions of each cant recorded, with all data being recorded by log number. The database contains over 4,600 logs of data.

In collaboration with the Appalachian Hardwood Manufacturer’s Association, the AHC developed a set of Guidelines for Scaling and Grading of Hardwood Logs2 that are available for industry use. The following Grading Table (Figure 4) is contained in the aforementioned Guidelines. The grades are classified by scaling diameter and clear faces, with the proportion of Select & Better lumber used in assigning the grades. The applicable Select & Better proportions are listed at the bottom of Figure 4. For instance, a Prime grade log will have an estimated 55 percent or greater proportion of Select & Better lumber and a Grade 3 log will have less than 10 percent Select & Better lumber.

METHODS

For the purposes of this article a comparison will be made between sawing a pallet cant and boards versus sawing a railroad tie, for red oak and white oak logs. Five log grade combinations are used for illustration. Because the mills included in the database were more likely to saw pallet cants, the combinations selected were based in part on selecting diameter and clear face combinations with higher percentages of logs sawn into tie sized material. The five log grade combinations are:

- 13-inch 0 clear faces (Grade No. 3, see Figure 4)

- 12-inch 1 clear face (Grade No. 3, see Figure 4)

- 13-inch 2 clear faces (Grade No. 2, see Figure 4)

- 14-inch 3 clear faces (Grade No. 1, see Figure 4)

- 15-inch 4 clear faces (Grade No. Select+, see Figure 4)

Database logs were divided into 2 categories for this analysis:

- Logs that only sawed out pallet cants (cross-sectional area of the cant <48 square inches). logs that sawed out a railroad tie or timber material only (cross-sectional area of the cant/tie/timber >=48 square inches). This allows for consideration of 6” x 8” railroad ties in the analysis.

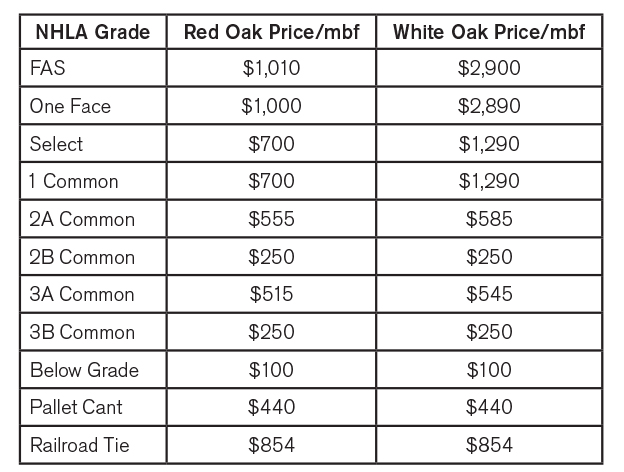

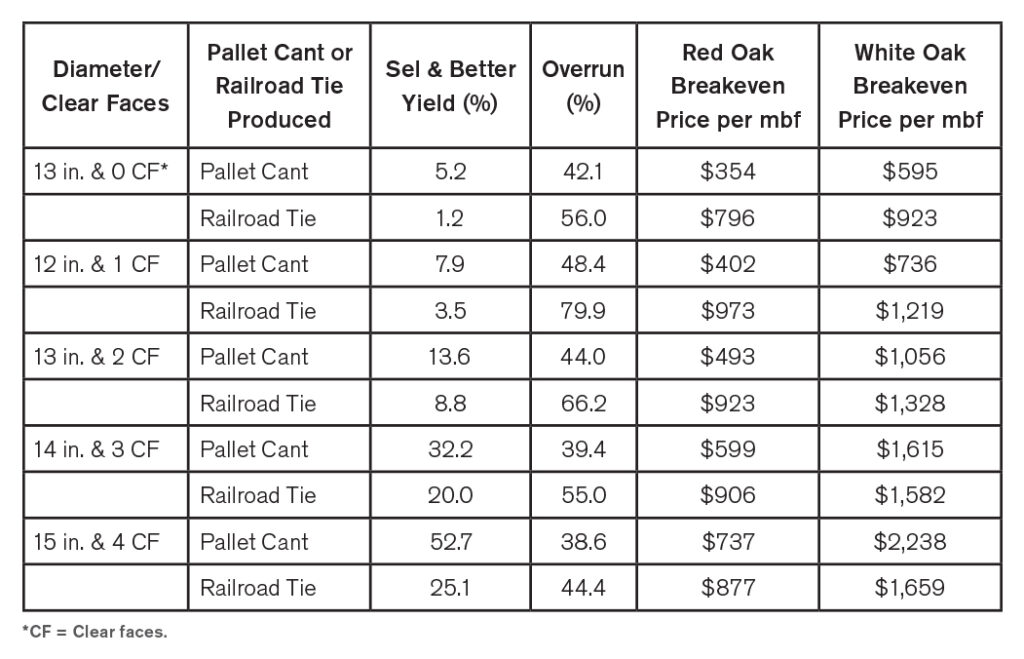

- Lumber and cant/tie prices are from a variety of sources and the prices used in the analysis are included in Table 1.

Sawing cost is assumed to be $250/mbf and there is no profit consideration, resulting in breakeven pricing of logs to compare the two sawing strategies. That is, the breakeven price indicates what the mill could pay for logs delivered to the mill and not make or lose money on the transaction. Note, Select lumber is priced as 1 Common lumber and both 2B Common and 3B common lumber are priced as random width pallet lumber. Below Grade (BG) lumber is priced at $100 per mbf.

RESULTS

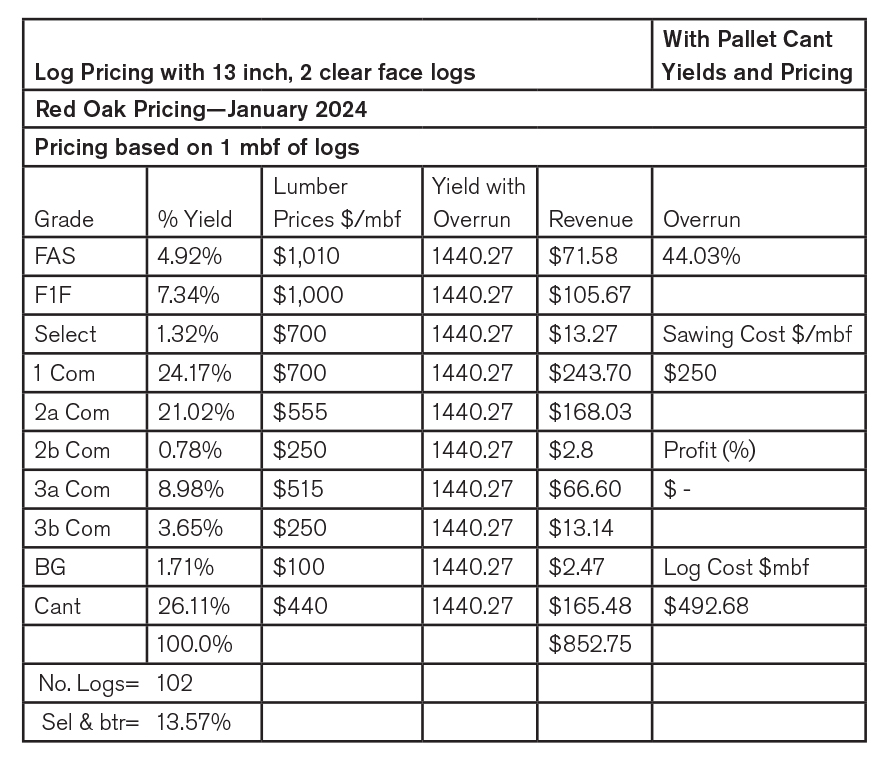

The log combination of 13 inches scaling diameter and 2 clear faces is used to illustrate the analysis, specifically for sawing a pallet cant plus boards, in Table 2.

As indicated in Table 2, the analysis is based on 1 mbf of logs, Doyle scale. The first column identifies the NHLA grade, the second column provides the grade yields (based on the data collected by AHC). The third column provides lumber and cant pricing for January 2024 (Table 1), while column four provides the yield with overrun. The fifth column entries are determined by multiplying the percentage yield (column 2 in decimal form) times the lumber/cant price (column 3) times the yield with overrun (column 4) divided by 1,000, to provide the revenue for each lumber grade.

The breakeven log cost is determined to be $492.68 per mbf, with a Select & Better yield of 13.6 percent and an overrun of 44.03 percent.

Table 3 provides a summary of the results for the 5 combinations of scaling diameter and clear faces for both red oak and white oak. For the case of 13-inch, 2 clear face logs, the breakeven price for sawing ties from red oak is $923 per mbf versus the $493 per mbf for sawing a pallet cant and boards. The reason for this is that the railroad tie option accomplishes two things: increases overrun by over 22 percent from 44.0 percent to 66.2 percent and applies a significantly higher price to the tie than to the pallet cant (almost double from $440 per mbf to $854 per mbf). On the other hand, the production of Select & Better lumber is higher for the pallet cant/board option (13.6 percent) than the railroad tie option (8.8 percent). However, this difference does little to offset the increase in overrun and the accompanying price of railroad ties. In this particular market scenario, it is always better to saw a railroad tie than to saw a pallet cant and boards.

For all the red oak options summarized in Table 3, it is more profitable to saw a railroad tie than a pallet cant and boards. It is important to note that as log diameter and the number of clear faces increases, the margins in favor of the railroad tie option decreases. For instance, the 15 inch, 4 clear face difference in breakeven prices shrinks to $140 per mbf. This is primarily due to the increased percentage of higher grade lumber.

In the case of white oak, (while the grade yields and overrun are the same as red oak, the AHMI grading system, like individual mill grading systems, treats logs of a given diameter and clear faces the same in terms of lumber grade yields and overrun and differentiates based on species and price), lumber pricing has a much greater impact on breakeven pricing and therefore the return to the mill.

Thus, Table 3 presents a somewhat different picture for white oak. For the 2 clear face and poorer logs, the outcome is the same as with red oak; the best option is to saw and market a railroad tie. However, for the 14-inch, 3 clear face and 15-inch 4 clear face logs the better option is to saw a pallet cant and boards. For these two diameter/clear face combinations (highlighted in Table 3), the production of Select & Better lumber offsets any advantage in overrun and tie price, as the Common and Better lumber pricing dominates.

SAWING COST

It is important to provide a caveat with respect to sawing cost. Because this analysis uses cost/mbf to develop breakeven costs, one should be aware of the impact this has. The sawing cost in this analysis is calculated from the board footage produced from one thousand board feet of logs (Doyle scale). Therefore, the railroad tie option results in a higher sawing cost because of the higher overrun, when in fact the cost should be lower because the number of sawlines is fewer and the time to process through the mill is less. The more accurate sawing cost would be based on the time it takes to process a log through the mill times the cost per unit time. Of course, this requires more detailed analysis of sawing times, which few mills have undertaken.

The upshot of this anomaly is that the railroad tie option is penalized, resulting in a lower breakeven price. The impact can be illustrated with the 14-inch, 3 clear face, white oak logs. The difference in breakeven price is $33 per mbf ($1,615 vs. $1,582). While it is not necessarily an accurate assumption, using the sawing cost difference between the two options and adding it to the breakeven price of the railroad tie option results in an additional $39 per mbf to the tie option, bringing the BE price to $1,621 per mbf vs. $1,615 per mbf, essentially a toss-up in terms of choice.

CONCLUSION

Obviously, the selection of sawing strategies should be a dynamic process where all the factors are routinely updated, in order to maximize revenue to the mill. As lumber and cant/tie prices change mills should revisit their sawing strategies. From an historic perspective, railroad tie production has been a reasonable option for mills, especially when grade lumber markets are depressed and even when grade markets are stable because of the impact of railroad tie vs. pallet pricing, combined with superior overruns with railroad ties.

Footnotes

1 HMR. 2001–2023. Hardwood Market Report: Various Volumes and Issues. HMR, Memphis, Tennessee.

2 Appalachian Hardwood Manufacturers, Inc. 2019. Guidelines for the Scaling and Grading of Hardwood Logs. Appalachian Hardwood Manufacturers, Inc., High Point, NC. 14pp.

{kind=link}