INTRODUCTION

There is a strategic choice for hardwood sawmills between selling a railroad tie versus sawing that tie into a pallet cant and boards. The key consideration is whether, once a tie sized piece is reached, is it better to saw one or more boards from the tie or leave it as is. The downside of taking one or more boards is the loss of volume due to kerf, the cost of additional sawlines, the likely reduction in value for the residual cant, oversizing of the board to meet target thickness, loss of volume due to the length difference, and any waste due to unused volume that is simply lost in the process. The revenue potential lies in producing board(s) with enough value to offset the associated costs.

METHODOLOGY

In mathematical form, the economic decision whether to saw a pallet cant and additional boards from a railroad tie can be analyzed as follows:

BEP = (P1C1 – P2C2 + SC * Bn)/Bn

where,

BEP = the breakeven price for the additional board(s) ($/MBF),

P1 = the price per mbf of the larger cant (a railroad tie in this case) ($/MBF),

C1 = the volume, in mbf, of the larger cant/tie,

P2 = the price per mbf of the smaller cant ($/MBF),

C2 = the volume, in mbf, of the smaller cant,

SC = the cost of n additional sawlines or sawing cost per mbf,

Bn = the additional volume of n boards, in mbf, and

n = 1, 2, 3, or more boards

The BEP (breakeven price) represents the value required of the additional boards in order for the total value of the pallet cant and additional boards to match the value of the railroad tie.

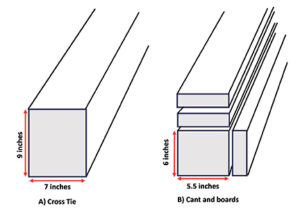

The critical decision occurs when the target cant/tie size has been reached and the opportunity to saw one or more additional boards from a tie or timber (or even from a larger pallet cant to a smaller pallet cant) is available. A common situation is a railroad tie with width/thickness of 7” x 9”, 6” x 8”, or 7” x 8” and the next target size is a pallet cant, with the most common sizes being 3.5” x 6”, 4” x 6”, 5.5” x 6”, and 6” x 6”. The same type of decision would apply for sawing additional boards from a timber-sized product (with a cross sectional area greater than 63 square inches (i.e., 7” x 9”)), resulting in a pallet cant or perhaps a railroad tie. However, timbers are bought and sold in a range of sizes, with a wide range of options for sawing one or more additional boards, but the same concept presented here could also apply to timbers.

A number of options are possible for the actual breakdown of the tie into a cant and boards. First, different kerf widths for the additional sawlines are possible, depending on the equipment configurations across mills. If the breakdown occurs solely on a circular headrig then the kerf could be assumed to be ¼ inch. If the breakdown occurs on a band headrig or resaw, then the kerf will most likely be less than ¼ inch.

When producing additional boards from a tie or timber, it is important to maintain board width at or above 6 inches, in order to preserve the possibility of an FAS/F1F board. For illustration purposes consider a 7” x 9” railroad tie with a possible breakdown of two 7”, 4/4 boards from the two 7” faces of the tie, followed by one 6”, 4/4 board from one of the adjacent 6” faces, resulting in a 5.5” x 6” pallet cant. Then, assuming a target board thickness of 1-1/8 inches and a kerf of ¼-inch the total thickness required to remove the two 7-inch boards is 1-1/8 inch + ¼-inch for board 1 and 1-1/8 inch + ¼-inch for board 2, totaling 2-¾ inches and leaving a 6-¼ inch residual cant. This residual width could be removed in a shim cut (a cut to remove a small amount of wood in order to properly size the cant), could simply remain on the cant (assuming the cant buyer specifications allow for the additional thickness) or one of the boards could be sawn as a 5/4 board. Or alternatively, for a thinner kerf using a resaw the possibility may exist for manufacturing two (2) 5/4 boards.

Similarly, for the 6-inch board and a ¼-inch kerf, the overall thickness required is 1-1/8 inch + ¼-inch kerf or 1-3/8 inch, resulting in a 5-5/8-inch cant. The excess 1/8-inch could be removed in a shim cut or simply remain on the cant, assuming the cant buyer specifications (tolerances) allow for the additional thickness.

There are at least two options when specifying sawing costs. First, for mills that turn the log/cant on the headrig or on a resaw to produce one board at a time, the additional sawlines and associated cost must be considered when determining sawing cost. This can be accomplished in two ways. First, the mill’s sawing cost per mbf can be applied to the footage of the boards produced. The second way is to use the cost per sawline as the measure of the cost to remove the boards from the tie.

Second, for mills utilizing a gang saw to breakdown a flitch (a log sawn on two sides to create two flat surfaces), there is no additional sawing cost, as the boards to be removed from the tie are removed with all other boards in one or two passes, which requires no additional sawing cost as this is standard operating procedure. In this case, the variable SC in equation (1) can be set to zero.

DETERMINING BREAKEVEN PRICES

This sawing strategy requires a continuing assessment of the choice between sawing an extra board(s) or not, as quantified by equation (1). Equation (1) can be used to determine the best option over all the available choices and should be updated regularly, as prices change. As an example of how to use equation (1) assume the following, using prevailing lumber and cant prices from the Hardwood Market Report (August 2023)1:

- The decision is whether to saw three boards from a 7” x 9” railroad cross tie, resulting in two 7” boards and one 6” board, all 8-feet long and a residual pallet cant 8-feet in length.

- The value of the resulting 5.5” x 6” cant is $475 per mbf.

- The value of the 7” x 9” oak tie is $874 per mbf.

- The cost per mbf to run the mill, for purposes of this illustration, is assumed to be $300 per mbf.

To illustrate the calculations for determining what the boards produced from tie must yield in terms of market price, the following data is used, using August 2023 pricing:

Tie price = $874 per mbf

Tie Volume = 44.625 bf

Residual cant price (5.5” x 6” x 8’) = $475 per mbf

Residual cant volume = 22 bf

Volume of sawn boards = 13.333 bf

Sawing cost = $300 per mbf

BEP = ($874 * 0.044625mbf – $475 * 0.022 mbf + $300/mbf * 0.01333 mbf)/(0.01333 bf) = $2,442/mbf

So, in order to make the decision to saw the tie into boards and a residual cant, the boards to be sawn need to be of such a grade that their market value is at least $2,442 in order to breakeven on the decision to saw. Using August 2023 HMR pricing estimates for Appalachian Region lumber, no pricing of 1 Common or FAS, for any species, exceeds a price of $2,442 per mbf. In effect, there is no economic justification for sawing the tie into a pallet cant and boards.

In the case of a gang saw in the breakdown of a tie into a cant the equation, without sawing cost as a variable, the resulting BEP is:

BEP = ($874 * 0.044625 mbf – $475 * 0.022 mbf)/(0.01333) = $2,142

Again, no 1 Common lumber of any species exceeds a price of $2,142 and, again from the August 2023 HMR, only Walnut has FAS lumber prices exceeding $2,142 per mbf.

HISTORIC BREAKEVEN PRICES

It is important to consider an historic perspective for this analysis, as current pricing data may be anomalous. Pricing from 2017 through 2022, based on second quarter pricing is utilized (from HMR prices for ties and pallet cants). Table 1 provides the breakeven results from the historical perspective. Over the period, breakeven pricing varied up to $289 per mbf.

Table 2 provides market prices for red and white oak for the period of 2017 to 2022 as a measure of whether it is economical to saw the railroad tie into a pallet cant and boards, from an historical perspective.

In the case of red oak, there is no market price that justifies sawing the 7” x 9” railroad tie into a pallet cant and boards, as the breakeven price exceeds all options. For white oak, the period of 2021 to 2022 did offer a possible option to saw a pallet cant and boards (as highlighted in yellow in Table 2). However, it must be noted that in 2021 all three boards would have to grade out as FAS, which is, from a practical perspective, nearly unattainable.

For the case of white oak in 2022, the two 7” boards could be 1 common and the 6” board could be FAS, resulting in a weighted price of $2,120 per mbf, well above the $1,786 per mbf breakeven (which is the worst case combination of grades for the three boards). Of course, the caveat is whether the two 1 Common and one FAS board can be sawn from the tie. In this particular case, with 2A Common at $935 per mbf, the decision becomes more favorable for a pallet cant and boards, as the breakeven price for one 7” FAS board, and the remaining two boards being 2A Common is $1,811 per mbf, slightly above the $1,786 per mbf (albeit with little profit margin).

DISCUSSION

A couple of additional issues are at play here. One is that a railroad tie can only be sawn effectively from logs of a certain size. For 7” x 9” ties it is generally thought that logs at least 13-inches in diameter are necessary. Other tie sizes may be possible from smaller diameter logs (i.e., 7” x 8” and 6” x 8”).

Second, an accompanying challenge is getting loggers to cut 9-foot logs, plus a trim allowance, to at least allow for the production of 9-foot boards through the mill or to cut 8 foot logs with sufficient trim allowance to saw a tie. In the former case, mills should consider scaling and paying the appropriate log scale for 9 foot logs (with sufficient trim).

Third, by marketing the tie, a mill can generally reduce the number of low grade boards being produced, thereby eliminating some of the issues related to marketing low-grade lumber.

An additional possibility for mills that have traditionally been uninterested in purchasing lower quality logs (logs with 1 or 0 clear faces) would be to purchase these logs with the sole intent to saw and market railroad ties. The specifications for such logs would be 9 feet with a trim allowance and minimal sweep and crook and no holes, scaled as 9-foot logs with a minimum scaling diameter (e.g., 13 inches). In West Virginia with active markets for 9-foot yellow-poplar peelers, the move to 9-foot logs in other species should not be a significant issue.

There are numerous scenarios for sawing ties and timbers into pallet cants and boards and this is just one example. Using this approach with these other scenarios could be easily analyzed.

It is also important to remember that, given the standard tie volume of 44.625 bf, by choosing to saw the tie into a pallet cant and boards, the resulting volume of the residual cant (22 bf) and the 3 boards (13.33 bf) that are manufactured effectively reduces marketable volume to 35.33 bf (a 20.8% loss). With a 20.8% loss in volume, it is difficult to recover sufficient value to match the value of the railroad tie.

CONCLUSIONS

This analysis has illustrated that for most commercial hardwoods over the past six years, the decision to market a tie instead of a pallet cant and boards makes good economic sense, based on product pricing. Moving forward, mills should regularly update tie, pallet cant, and board pricing strategies to determine the most economically favorable option.

In Part 2 of this series, we will look at specific combinations of scaling diameter and clear face logs to further evaluate whether it makes economic sense to have a strategic objective of sawing and marketing railroad ties over some portion, if not all of a mill’s purchased logs. Effectively, mills may find it more lucrative to adjust their purchased log strategy to include different mixes of high and low grade logs depending on market conditions.

{kind=link}